The mortgage industry in 2026 faces unprecedented competition and evolving consumer behaviors. Mortgage professionals who rely solely on referrals or outdated marketing tactics struggle to maintain consistent pipeline velocity. This reality has created explosive demand for mortgage lead companies that deliver pre-qualified prospects ready to engage with loan officers. The sophistication of these specialized providers has evolved dramatically, transforming from simple contact list vendors into strategic growth partners leveraging AI, predictive analytics, and multi-channel acquisition strategies. Understanding how to evaluate, partner with, and maximize returns from these companies separates thriving mortgage businesses from those fighting for survival.

The Evolution of Mortgage Lead Companies in 2026

Traditional mortgage lead generation relied heavily on basic web forms and generic advertising campaigns. Today's mortgage lead companies operate with completely different methodologies that reflect technological advancement and consumer sophistication.

Modern lead providers now implement:

- Advanced AI qualification systems that predict conversion probability

- Real-time verification processes ensuring data accuracy

- Multi-touch nurturing sequences before lead handoff

- Integration capabilities with existing CRM platforms

- Transparent tracking and attribution modeling

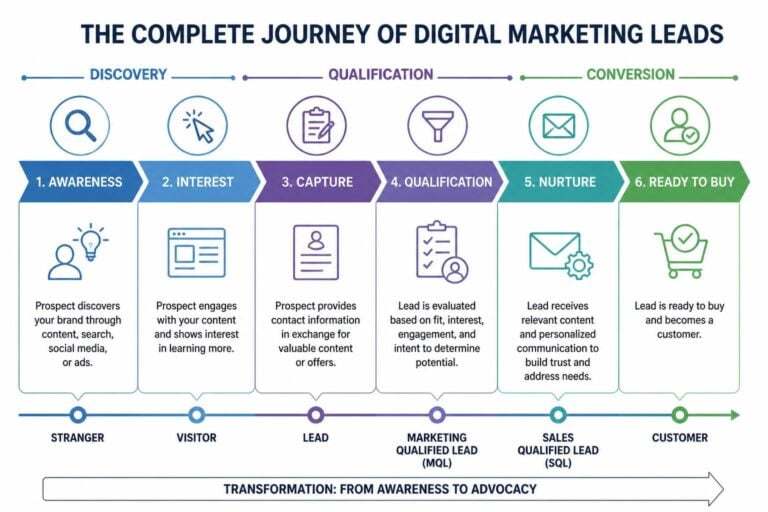

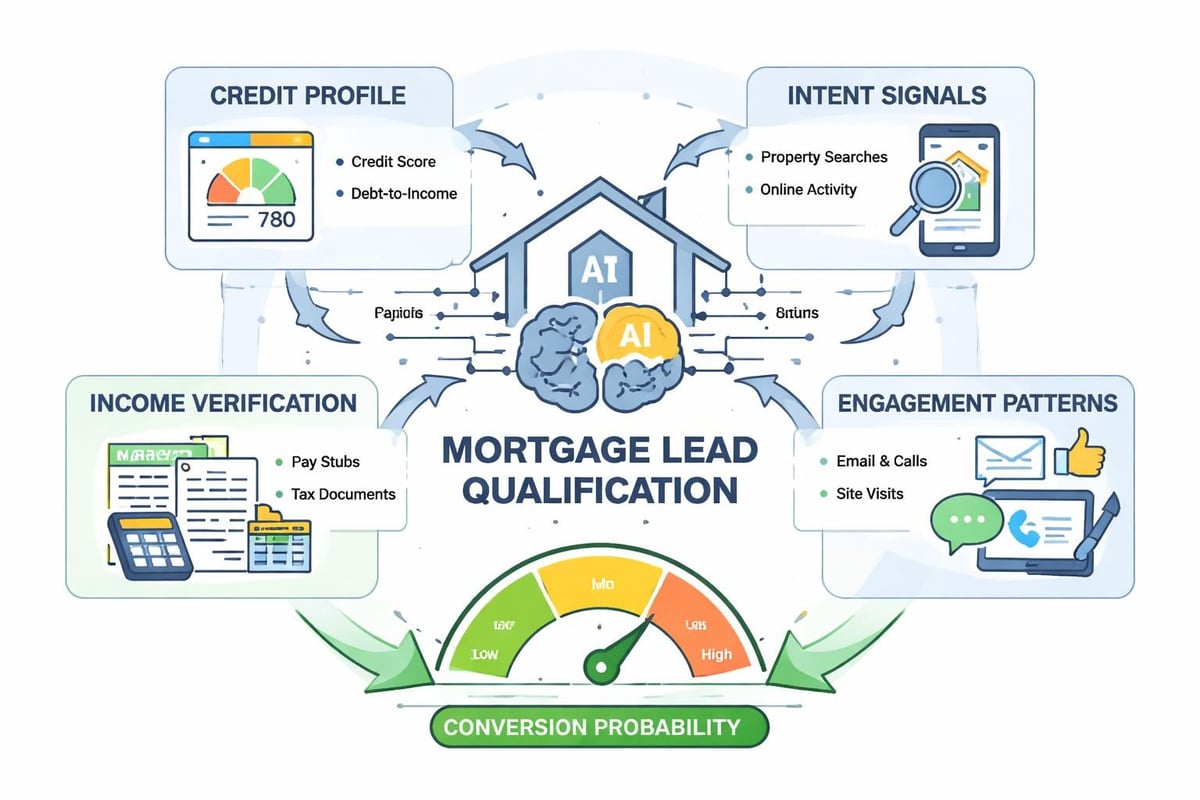

The shift toward lead generation with AI has fundamentally changed how qualified prospects enter your pipeline. Instead of receiving cold contacts who filled out a form five days ago, mortgage professionals now access leads that have been pre-engaged, verified, and nurtured through automated sequences.

This transformation addresses the critical pain point that plagued earlier generations of lead services: quality inconsistency. When you purchase leads that haven't been properly vetted or warmed, your team wastes countless hours chasing dead ends. The best mortgage lead companies in 2026 understand that their success depends entirely on your success, creating alignment that previous vendor relationships lacked.

Quality Metrics That Actually Matter

Not all mortgage leads carry equal value. The distinction between a $20 lead and a $200 lead often determines your profitability. Understanding the specific criteria that define lead quality empowers you to make strategic vendor decisions.

| Quality Factor | Premium Leads | Standard Leads | Low-Quality Leads |

|---|---|---|---|

| Response Time | Under 5 minutes | Under 2 hours | 24+ hours |

| Verification Status | Verified income & credit | Email verified only | Unverified |

| Exclusivity | Sold once | Sold to 3-5 buyers | Sold to 10+ buyers |

| Intent Level | Active application started | Information gathering | Passive browsing |

| Average Conversion | 18-25% | 8-12% | 2-5% |

Platforms like Private Mortgage Leads demonstrate how AI-powered systems deliver qualified real estate investment loan leads with guaranteed FICO scores and specific loan amounts. This level of precision eliminates the guesswork that traditionally plagued lead acquisition strategies.

The mathematical reality becomes clear when you calculate cost per funded loan rather than cost per lead. A $200 premium lead that converts at 20% costs $1,000 per funded loan. A $20 standard lead that converts at 3% costs $667 per funded loan, but requires significantly more time investment. Premium leads often deliver superior ROI when you factor in labor costs and opportunity costs.

Strategic Selection: Choosing the Right Partner

The marketplace for mortgage lead companies has become crowded with providers making bold promises. Your selection process should follow rigorous evaluation criteria that protect your investment and maximize outcomes.

Essential Evaluation Framework

Financial alignment represents the foundation of successful partnerships. Companies offering performance-based models or guaranteed results demonstrate confidence in their delivery. Traditional pay-per-lead structures create misaligned incentives where the vendor profits regardless of your conversion rates.

Services like SendLead’s mortgage lead delivery implement transparent five-step processes including financial modeling, funnel creation, customer targeting, and clear pricing structures. This transparency allows you to forecast expected returns before committing significant capital.

Technology integration capabilities cannot be overlooked in 2026. Your lead provider must seamlessly connect with your existing systems. Manual data entry creates delays, introduces errors, and prevents real-time response that modern borrowers expect.

Ask potential partners these critical questions:

- What is your average lead-to-funded conversion rate across all clients?

- How do you verify lead quality before delivery?

- What recourse do I have for non-performing or fraudulent leads?

- Can you provide references from mortgage professionals in my market?

- What happens if leads don't meet specified criteria?

The companies that hesitate or provide vague answers to these questions should be immediately disqualified from consideration. Top-tier providers welcome scrutiny because their performance validates their claims.

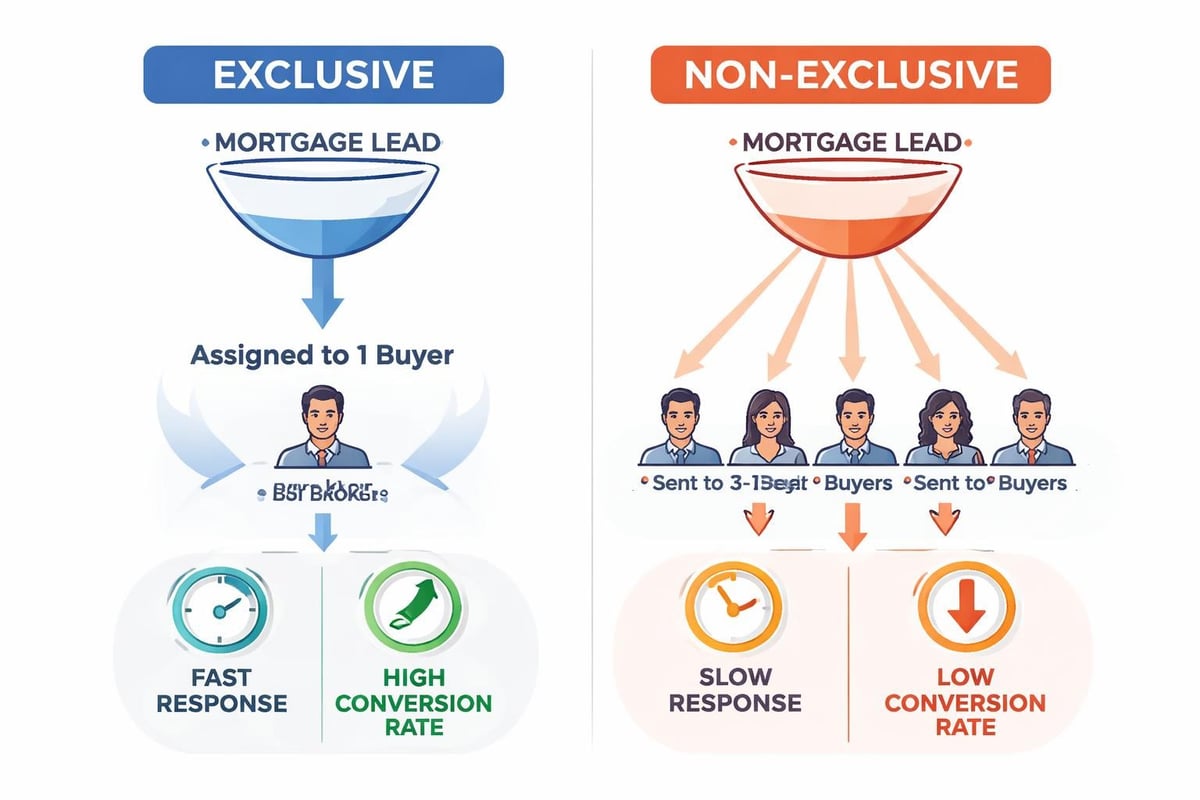

Exclusive vs. Non-Exclusive Lead Models

This decision significantly impacts your conversion rates and competitive positioning. Lead Planet offers insights into both exclusive and non-exclusive lead options, helping loan professionals understand the trade-offs involved.

Exclusive leads arrive to you alone, eliminating immediate competition. You control the conversation timeline and aren't racing against three other loan officers. The premium pricing reflects this advantage, typically costing 3-5x more than non-exclusive alternatives.

Non-exclusive leads get distributed to multiple buyers simultaneously. Speed becomes paramount. The first responder typically captures 35-40% of available conversions, while later responders fight for scraps. This model works best for teams with dedicated inside sales resources and automated response systems.

Your choice should align with your operational capacity. A solo loan officer without administrative support may find exclusive leads more manageable, while a team with rapid response capabilities can arbitrage non-exclusive lead pricing through execution excellence.

Maximizing ROI From Purchased Leads

Acquiring quality leads represents only half the equation. Your internal processes determine whether these opportunities convert into funded loans and satisfied customers. Mortgage lead companies deliver the raw material, but your systems create the outcomes.

Response Speed as Competitive Advantage

Research consistently demonstrates that response time correlates directly with conversion probability. Leads contacted within five minutes are 21 times more likely to qualify than those contacted after 30 minutes. This isn't marginal improvement; it's transformational difference.

Building systems that force leads to book sales calls creates predictable pipeline flow that doesn't depend on manual outreach. Automation handles initial engagement while human expertise focuses on relationship building and closing.

Implement these immediate response strategies:

- Automated SMS confirmation within 60 seconds of lead delivery

- Pre-recorded video introduction sent via email

- Calendar booking link embedded in all initial communications

- CRM automation that triggers multi-channel contact attempts

- Backup assignment if primary loan officer doesn't respond within 10 minutes

Companies like Mortgage Leads 247 emphasize performance-based models that filter unqualified prospects, but even the highest-quality leads die without rapid, professional engagement.

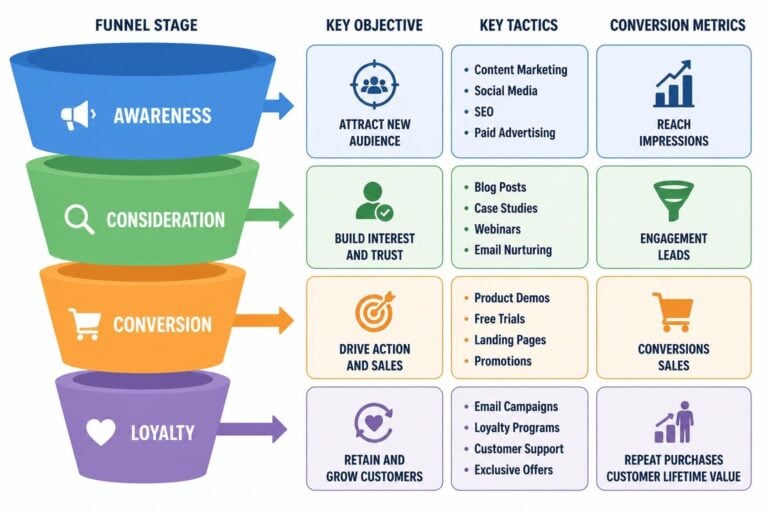

Nurturing Systems That Convert Over Time

Not every qualified prospect is ready to act immediately. The average mortgage borrower researches for 47 days before selecting a lender. Your nurturing system must maintain top-of-mind awareness throughout this decision journey.

Effective nurturing sequences include:

- Educational content addressing common mortgage questions

- Market updates showing rate trends and timing implications

- Social proof featuring recent client success stories

- Personalized insights based on their specific situation

- Low-pressure check-ins maintaining relationship warmth

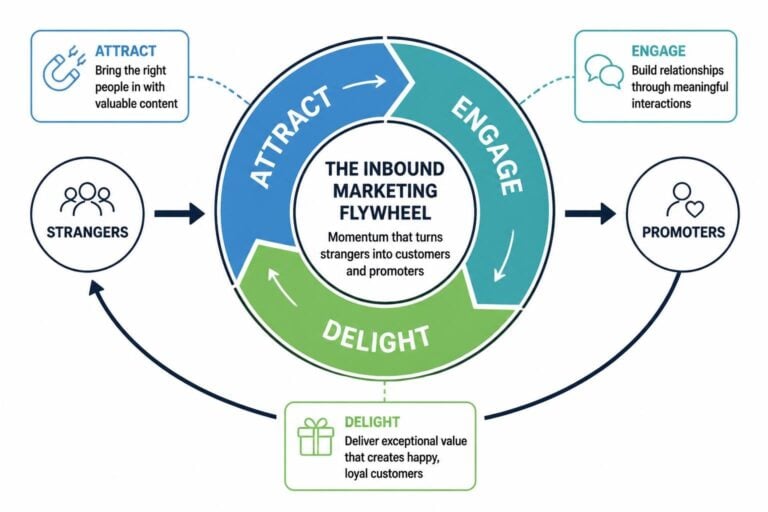

End-to-end marketing approaches recognize that lead generation represents just the beginning of customer acquisition. The journey from initial contact to funded loan requires orchestrated touchpoints that build trust, demonstrate expertise, and eliminate objections.

Industry-Specific Considerations for Different Mortgage Niches

Mortgage lead companies often specialize in particular segments of the lending market. Understanding these distinctions helps you select providers aligned with your business model and expertise.

Refinance vs. Purchase Leads

Market conditions in 2026 heavily influence which lead type delivers superior returns. Rising rate environments typically suppress refinance volume while purchase activity remains more stable. Your lead acquisition strategy should flex based on current market dynamics.

Refinance leads typically:

- Convert faster when rates are favorable

- Require less documentation and complexity

- Face higher competition from existing lenders

- Show more price sensitivity

Purchase leads typically:

- Involve longer sales cycles

- Create opportunities for realtor partnerships

- Require more educational content

- Generate higher lifetime value through future refinances

Providers like Camber Marketing focus on driving qualified mortgage leads that convert into new loans through proven direct mail pieces and data strategies, recognizing that different channels perform differently for various loan types.

Conventional, FHA, VA, and Specialty Products

Your product expertise should align with the lead sources you purchase. Attempting to convert VA leads without deep VA loan knowledge wastes both the prospect's time and your marketing investment.

| Loan Type | Average Lead Cost | Typical Conversion | Complexity Level |

|---|---|---|---|

| Conventional | $45-85 | 12-15% | Moderate |

| FHA | $35-65 | 10-14% | Moderate-High |

| VA | $55-95 | 8-12% | High |

| Jumbo | $125-250 | 6-10% | Very High |

| DSCR/Investor | $150-300 | 5-8% | Very High |

Specialty product leads command premium pricing because they target specific borrower profiles with unique needs. The Lead Gen emphasizes delivering exclusive and non-exclusive leads tailored to the specific lending products that brokers and banks offer, recognizing that mismatched leads create frustration on both sides.

Technology Integration and Data Management

Modern mortgage lead companies provide sophisticated data feeds that must integrate seamlessly with your technology stack. Poor integration creates bottlenecks that destroy the speed advantages that purchased leads should provide.

CRM and Lead Management Systems

Your customer relationship management platform serves as the central nervous system for lead processing. Every lead should automatically flow into your CRM with complete attribution data showing source, cost, and initial engagement metrics.

Essential CRM requirements include:

- Real-time API connections with lead providers

- Automated task creation for immediate follow-up

- Multi-channel communication tracking

- Performance reporting by lead source

- Duplicate detection preventing wasted outreach

Many mortgage professionals underestimate the importance of building a lead generation website that captures organic traffic alongside purchased leads. Diversification reduces dependence on any single source and improves overall cost per acquisition.

Attribution and Performance Tracking

Understanding which mortgage lead companies deliver actual funded loans versus superficial activity metrics determines your long-term strategy. Many providers tout impressive lead volumes while carefully avoiding conversion rate discussions.

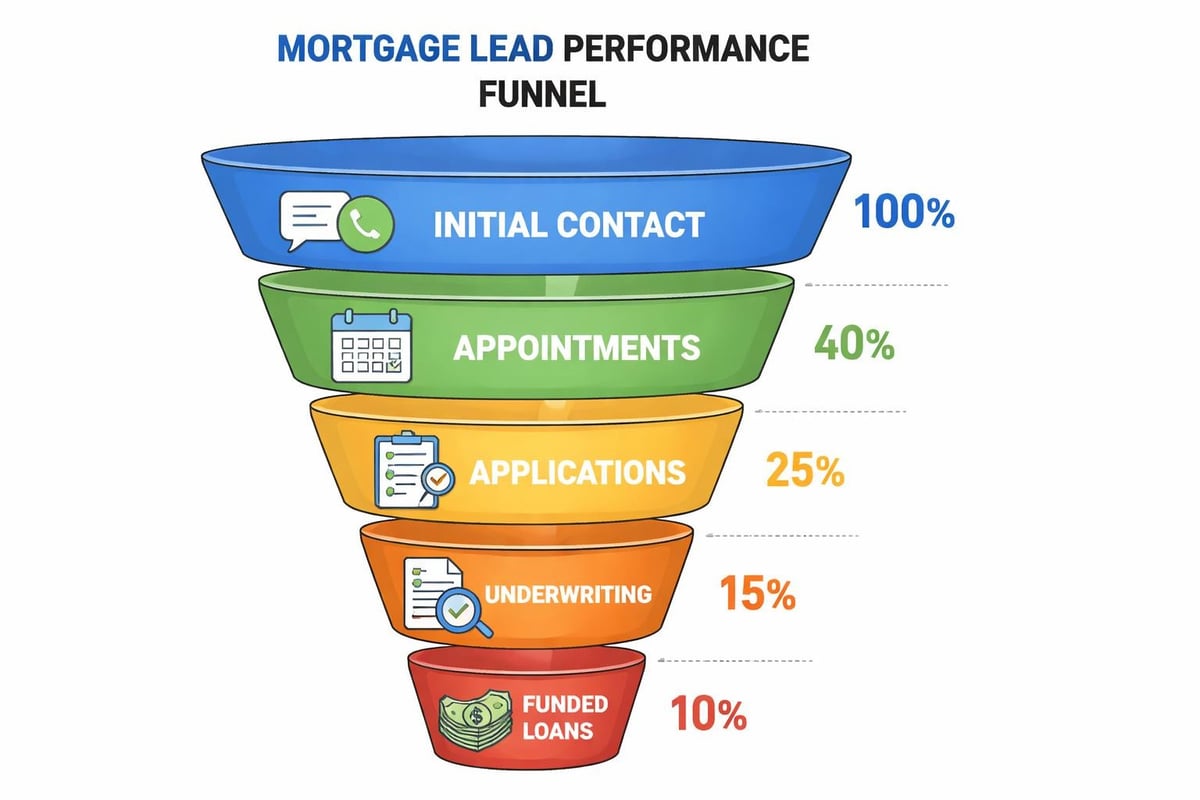

Track these critical metrics by provider:

- Lead-to-contact rate (what percentage actually answer the phone)

- Contact-to-appointment rate (qualification percentage)

- Appointment-to-application rate (serious intent confirmation)

- Application-to-clear-to-close rate (underwriting success)

- Funded loan percentage (ultimate success metric)

Only by analyzing the complete funnel can you determine true cost per funded loan. A provider delivering 100 leads monthly at $50 each might outperform one delivering 50 leads at $100 if the conversion rates favor the higher-volume source.

Compliance and Regulatory Considerations

The mortgage industry operates under strict regulatory oversight that extends to lead generation activities. Partnering with mortgage lead companies that cut corners on compliance exposes you to significant legal and financial risk.

TCPA and Do Not Call Regulations

The Telephone Consumer Protection Act imposes severe penalties for unsolicited contact. Your lead providers must obtain proper consent before delivering contact information. Written consent for automated calls and texts isn't optional; it's legally required.

Reputable providers include:

- Timestamped consent records for every lead

- IP address and device information from form submissions

- Clear disclosure language shown to prospects

- Opt-out mechanisms honoring Do Not Call registrations

Companies like Boom Sourcing emphasize advanced tools and trained agents to deliver high-quality leads while maintaining compliance standards. This attention to regulatory requirements protects both the provider and the loan officer from costly violations.

Fair Lending and Equal Credit Opportunity

Your lead acquisition strategies must comply with fair lending laws prohibiting discrimination. Targeting or excluding prospects based on protected characteristics creates liability regardless of whether you or your lead provider implemented the discriminatory practice.

Review these compliance elements:

- Geographic targeting that doesn't create redlining patterns

- Marketing language avoiding discriminatory implications

- Equal treatment of all leads regardless of demographic signals

- Documentation demonstrating consistent qualification criteria

Regulatory enforcement in 2026 has intensified, with agencies using advanced analytics to identify suspicious patterns. The mortgage lead companies that survive and thrive maintain robust compliance programs that protect their clients.

Cost Structure and Pricing Models

Understanding how mortgage lead companies price their services reveals their confidence in product quality and alignment with your success. The pricing model often matters more than the absolute price point.

Pay-Per-Lead vs. Performance-Based Pricing

Traditional pay-per-lead pricing creates misaligned incentives. The vendor gets paid whether you close loans or not. This model works when quality remains consistently high, but provides no recourse for underperforming leads.

Pay-per-lead advantages:

- Predictable budgeting and cost forecasting

- Simple accounting and tracking

- Wide provider selection

- Lower barrier to entry for testing

Performance-based advantages:

- Vendor accountability for conversion outcomes

- Risk sharing between provider and loan officer

- Quality incentives naturally aligned

- Higher confidence in provider capabilities

Trident Affinity Group describes utilizing AI technology to connect with individuals seeking mortgage services, creating efficiency that enables performance-based arrangements. When providers invest in sophisticated qualification systems, they can confidently tie pricing to outcomes rather than activity.

Hidden Costs and True ROI Calculation

The advertised price per lead rarely represents your total acquisition cost. Factor in these additional expenses when evaluating mortgage lead companies:

- Lead replacement costs when quality standards aren't met

- Technology integration and API connection fees

- CRM licensing if provider requires specific platforms

- Staff time for follow-up and nurturing activities

- Opportunity costs from pursuing unqualified prospects

A complete ROI analysis compares total investment against funded loan revenue. If you spend $5,000 monthly on leads and fund four loans with average revenue of $3,500, your ROI calculation shows $14,000 revenue against $5,000 investment plus staff time. This framework reveals whether you're building a sustainable growth engine or subsidizing an expensive lead generation experiment.

Alternative and Complementary Strategies

While mortgage lead companies provide valuable prospect flow, diversification reduces risk and often improves overall cost per acquisition. The most successful mortgage professionals blend purchased leads with other generation methods.

Organic Lead Generation

Building your own lead generation capacity creates owned assets that compound over time. Unlike purchased leads that disappear when you stop paying, organic channels deliver ongoing returns from past investments.

High-performing organic strategies include:

- SEO-optimized content targeting mortgage-related searches

- YouTube educational videos answering common questions

- Social media engagement building community and authority

- Email list nurturing of past prospects and clients

- Referral programs incentivizing current client advocacy

The challenge with organic approaches lies in the time investment required before meaningful results appear. Most mortgage professionals need immediate pipeline flow, making purchased leads valuable while organic channels mature. Understanding best marketing platforms helps you allocate resources across the most effective channels for your specific market.

Strategic Partnerships

Real estate agent relationships have historically provided mortgage professionals with high-quality purchase leads at zero direct cost. These partnerships require cultivation and value delivery but create competitive moats that purchased leads cannot replicate.

Develop realtor partnerships through:

- Co-marketing programs sharing acquisition costs

- Fast closing guarantees making agents' jobs easier

- White-glove client experience generating repeat referrals

- Educational workshops demonstrating expertise

- Technology tools streamlining the transaction process

Combining relationship-driven leads with purchased leads from mortgage lead companies creates balanced pipeline sources that weather market changes and competitive pressures.

Emerging Trends Reshaping the Industry

The mortgage lead generation landscape continues evolving rapidly. Staying ahead of these trends positions you to capitalize on opportunities before they become commoditized.

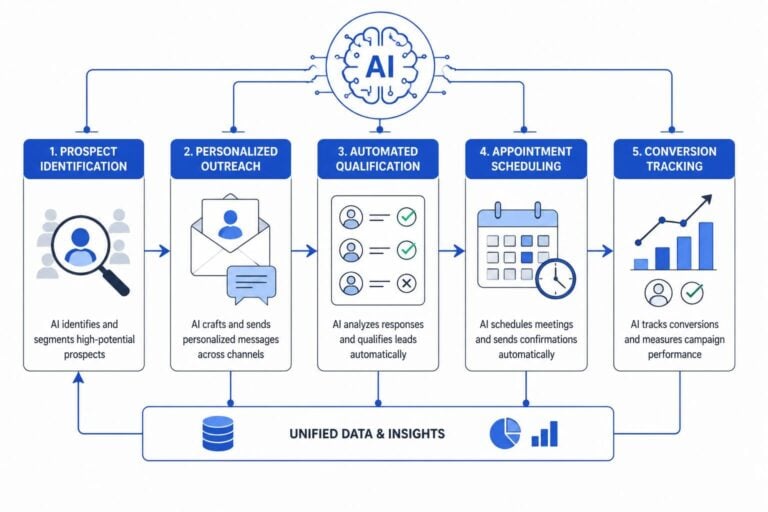

Artificial Intelligence and Predictive Analytics

AI systems now predict which prospects will convert with remarkable accuracy. By analyzing thousands of data points including credit behavior, online activity, demographic factors, and engagement patterns, these systems score leads more effectively than human judgment alone.

Forward-thinking providers implement:

- Behavioral scoring predicting conversion probability

- Automated nurturing sequences adapting to engagement levels

- Optimal contact timing based on individual patterns

- Personalized content matching specific borrower situations

- Predictive modeling forecasting pipeline velocity

The integration of AI into lead generation strategies represents the most significant advancement in mortgage marketing over the past decade. Providers leveraging these capabilities deliver measurably superior results compared to those relying on traditional methods.

Multi-Channel Attribution and Customer Journey Mapping

Modern borrowers interact with multiple touchpoints before selecting a lender. They might see your Facebook ad, visit your website twice, receive an email, and then submit a lead form through a partner site. Understanding this journey informs smarter marketing investment.

Advanced mortgage lead companies track:

- Initial awareness source and message

- Research behavior and content consumed

- Comparison shopping patterns

- Decision triggers and timing factors

- Post-close satisfaction and retention opportunities

This granular visibility enables optimization that simple lead-to-close tracking cannot achieve. You discover which channels assist conversions even when they don't receive last-click attribution, preventing the premature abandonment of valuable marketing investments.

Vendor Management and Relationship Optimization

Your relationship with mortgage lead companies shouldn't be transactional. The best providers function as strategic partners invested in your long-term success rather than vendors extracting maximum short-term revenue.

Performance Reviews and Continuous Improvement

Schedule quarterly business reviews with your lead providers to analyze performance trends and identify optimization opportunities. These discussions should examine conversion metrics by lead source, time periods, loan products, and marketing channels.

Productive review agendas include:

- Detailed conversion funnel analysis

- Lead quality trend identification

- Pricing and volume optimization discussions

- Integration improvement opportunities

- Market condition impacts and strategy adjustments

Providers who resist these conversations likely lack the performance data to support their claims. Premium partners welcome scrutiny because it drives mutual improvement and strengthens the relationship.

Negotiation Leverage and Contract Terms

As you scale lead purchases and demonstrate consistent conversion performance, you gain negotiation leverage for improved pricing, priority access, or custom arrangements. Most mortgage lead companies reserve their best terms for high-volume, long-term clients.

Negotiate these favorable terms:

- Volume discounts based on monthly spend commitments

- Performance guarantees with replacement or refund policies

- Exclusive territory rights preventing local competition

- Custom lead criteria matching your ideal borrower profile

- Flexible pricing during seasonal volume fluctuations

Document all agreements explicitly in written contracts. Verbal promises become worthless when account representatives change or company ownership transitions occur.

Building Internal Capacity to Maximize Lead Value

The most sophisticated mortgage lead companies can only deliver prospects. Your internal systems determine whether those prospects become funded loans and delighted clients. Investment in lead generation without corresponding investment in conversion infrastructure wastes money.

Sales Training and Script Development

Your team's communication skills directly impact conversion rates. Generic, product-focused conversations bore prospects and fail to address their specific concerns. Consultative approaches that diagnose needs before prescribing solutions dramatically outperform traditional sales tactics.

Effective training programs cover:

- Discovery questioning techniques uncovering true motivations

- Objection handling frameworks addressing common concerns

- Storytelling methods making complex information accessible

- Closing strategies creating natural next steps

- Relationship maintenance ensuring long-term satisfaction

Recording and reviewing actual sales conversations reveals improvement opportunities that theoretical training alone cannot address. The mortgage professionals who consistently convert at 20%+ rates do specific things differently than those converting at 8%.

Technology Stack Optimization

Your ability to respond instantly, track comprehensively, and communicate professionally depends entirely on your technology infrastructure. Outdated systems create friction that kills conversions.

Essential technology components include:

| System Category | Minimum Requirement | Premium Recommendation |

|---|---|---|

| CRM Platform | Basic contact management | AI-powered lead scoring |

| Communication | Email and phone | Multi-channel automation |

| Documentation | Manual file storage | Cloud-based collaboration |

| Application Processing | Paper-based | Digital with e-signature |

| Analytics | Spreadsheet tracking | Real-time dashboards |

The technology investments that seem expensive in isolation become bargains when measured against improved conversion rates and reduced labor costs. A $500 monthly software investment that improves conversions by 3% easily generates 10x returns for most mortgage professionals.

Mortgage lead companies represent powerful growth accelerators when selected carefully and managed strategically. The difference between mediocre results and exceptional outcomes lies not in the leads themselves, but in your evaluation criteria, internal processes, and conversion infrastructure. By implementing the frameworks outlined above, you transform purchased leads from expensive experiments into predictable revenue engines. If you're ready to build automated systems that generate qualified mortgage leads and convert them into funded loans without the trial-and-error typical of traditional approaches, Adstra provides guaranteed growth partnerships that align our success with yours, leveraging AI technology to deliver the qualified prospects your business needs to thrive in 2026's competitive marketplace.